What is the interest rate forecast for 2024? Is the Euribor expected to fall? What are the conditions of bank financing in this context?

Below, we share with you the opinions of analysts who answer these questions. In addition, we also show you what the rise in interest rates means for business financing.

Índice

Economic situation and forecasts for interest rates in Spain

Taking into account the development of inflation, the main macroeconomic indicator that affects the evolution of interest rates, we observe that it began to moderate in mid-2022 and has maintained a downward trend throughout 2023, with a slight rebound in the 4th quarter of the year.

Specifically, the interannual CPI stood at 3.1% in December 2023, according to data from the Statistics National Institute.

Thus, inflation has managed to close 2023 with a lower rate than the two previous years, which gave rise to the European Central Bank to increase interest rates (causing the largest escalation in history).

Given the inflationary moderation, statements are beginning to be heard about stopping increases in interest rates from the European Central Bank. Leaving the price of money at 4.5%.

In fact, in its first meeting of 2024 the ECB kept rates at 4.5% for the third consecutive time. In any case, based on Christine Lagarde's statements, no declines are expected, at least during the first quarter of the year.

When will the Euribor go down?

The truth is that the Euribor is already showing signs of having hit a ceiling. A slight decline is observed from October 2023 and it is likely to see a slight correction during 2024 as a result of the suspension of interest rate increases.

Specifically, after the maximum produced in September (4.15%), the 12-month Euribor closed 2023 at 3.68%.

According to forecasts made by CaixaBank Research, the 12-month Euribor is expected to close 2024 at 3.06%.

In conclusion, it can be expected that interest rates on bank financing will not continue to increase, but will moderate significantly.

However, interests have been at historically high levels. Therefore, although they may suffer a contraction, it is most likely that they will continue at rates that make access to credit difficult and represent a high cost for companies that have to resort to debt.

What does the rise in interest rates mean for bank financing?

A higher cost of credit reduces the capacity for investment and business development.

However, the Quarterly report and macroeconomic projections

of the Spanish economy published by the Bank of Spain (December 2023) indicates that the economy maintains dynamism despite the fact that monetary policies continue to be restrictive.

However, it also refers to the relaxation in interest rate increases by developed economies (Europe and the United States, mainly).

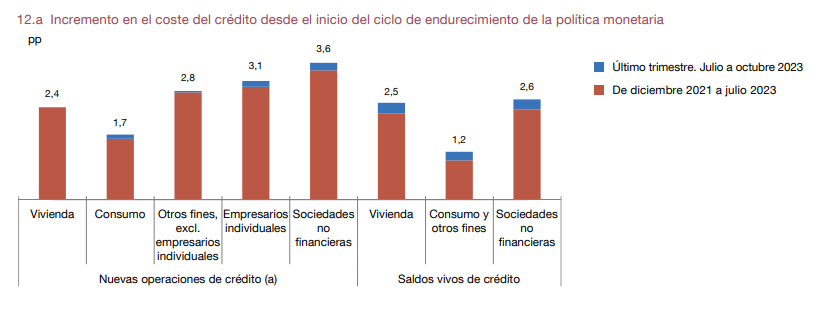

In this sense, the report shows how there has been a slowdown in Spanish economic activity in the third quarter of 2023 and how the cost of bank financing for households and companies has continued to increase in the last months of the year.

Source: Bank of Spain

In the Bank Loan Survey It clearly shows how during the third quarter of the year both the granting criteria and the conditions applied to new loans have been tightened (for 6 consecutive quarters).

In conclusion, despite a moderation in interest rate increases, bank financing still continues to maintain a restrictive trend. According to the aforementioned survey, it is mainly due to the risks perceived by financial entities, as well as a lower tolerance for it.

In this context, more and more companies are opting for alternative financing solutions.